Singapore HRMS and Payroll Software

One of the Best Fully Integrated Human Resource Management System

HRMS and Payroll Software Professional Services

|

Service Support We are able to troubleshoot specific technical errors and guide user to resolve common error via phone, online team viewer or on site service support. |

|

Data Migration Our experience programmer and support team will help to migrate your current in house systems via different migration technique to ensure all your historical data for current year fully transfer to MyPay. |

|

Implementation and Configuration Services Our consultants setting up necessary templates, integrated module to enable payroll software meet your requirement |

|

User Training Comprehensive training will be given with programs available for users at all levels. |

|

Warranty and Maintenance Smart Touch never leave you alone and promise to continuous serve our client with available program payroll software solution |

Singapore HRMS and Payroll Software Features

| User define Popup Payroll Reminder | I. Payroll Software reminder alert for probation due date, work permit expire date and user define alert field. II. Assist Payroll Software officer to avoid overdue issue and penalty offence by local authority. |

| Smart Mobile Application | I. Preview Salary thru Smart Mobile Application II. Allows employees to check current (Mid or End Month), historical statement in detail. III. Access via smartphone without frequent enquiry with HR Manager. |

| Multi User Network Access | I. Centralized manage payroll part for multi Company. II. Handle by more than 1 payroll officer in different plan. |

| Latest Technology | I. MS SQL Database avoid database corruption problem. II. Integrated Smartime Attendance Management System (TMS) as well as other module such as eLeave, eScheduling, e-OT Approval, etracking System under V1SOHO Architecture. |

| Simple and Easy to Manage Function | I. Friendly use command to add in, query and sorting data features. II. Prorate salary for new join and termination employee based on payroll period. III. Electronic file thru the major bank. IV. Build in report writer facilities user customize own report. V. Complaint to Statutory Requirement. |

Singapore HRMS and Payroll Software Specifications

| Operating System (Minimum Requirement) | – Windows XP, Windows Vista, Windows 7 32/64 Bit – Intel Duo Core or AMD ATHLON X2 or Higher, 2GB RAM – 16GB hard disk, LAN and Screen Resolution 1024 x 768 pixels or higher |

| Database | MS SQL Server 2005 Express or Above |

| Employee Headcount Limit | Minimum – 100, Maximum – Unlimited |

| Multi-user Access Network | Unlimited |

| Input Order | TMS / Excel Spread Sheet / Manual |

| Payment Mode | Normal Pay (Mid/End Month), Bonus Pay, Advance Pay and Other Pay |

| Overtime (OT) Support | Standard OT, Flat Rate OT and OT Ceiling |

| Pay Element Code | Unlimited Allowance and Deduction |

| Multi Company | Yes |

| Recurring Pay Element | Yes |

| CPF/IRAS | Yes |

| Remotely Access | Yes |

| Smart Mobile Application | Yes |

| Online Bank File Submission | Yes (DBS/POSB/OCBC/UOB) |

| Backup and Recovery | Yes |

| TMS Integration | Yes |

| Reports | Yes (More than 70 type of Report) |

| Report Writer | Yes |

Singapore HRMS and Payroll Software Report Types

General Reports

| Employee Listing | Work Permit Report |

| Employee Details | Service Day Report |

| Fix Allowance and Deduction Report | Basic Rate Progression Report |

| New Join Report | Career Progression Report |

| Probation Due Report | Installment\Loan Report |

| Confirmation Report | Installment\Loan Report in Details |

| Resign Report | HeadCount by Date |

| Retire Report | HeadCount by Gender |

| Birthday Report | HeadCount by Basic Wage |

| Passport Report | Bank Reports: Bank\Cash Listing |

Payslip Reports

| Payslip | Deduction Report |

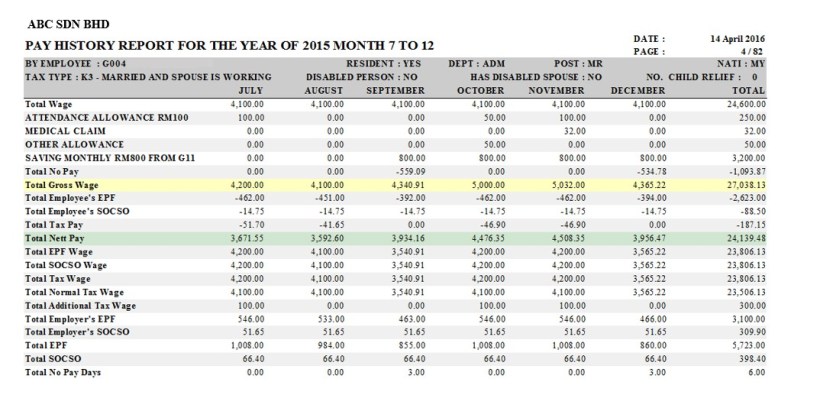

| Pay History Report | Reimbursement Report |

| Pay History Report (U) | Allowance & Deduction Report |

| Payroll Summary Report | Allowance & Deduction Report 2 |

| Payroll Summary Report in Details | Allowance Report |

| Payroll Summary Report in Details (Group) | Variance Report |

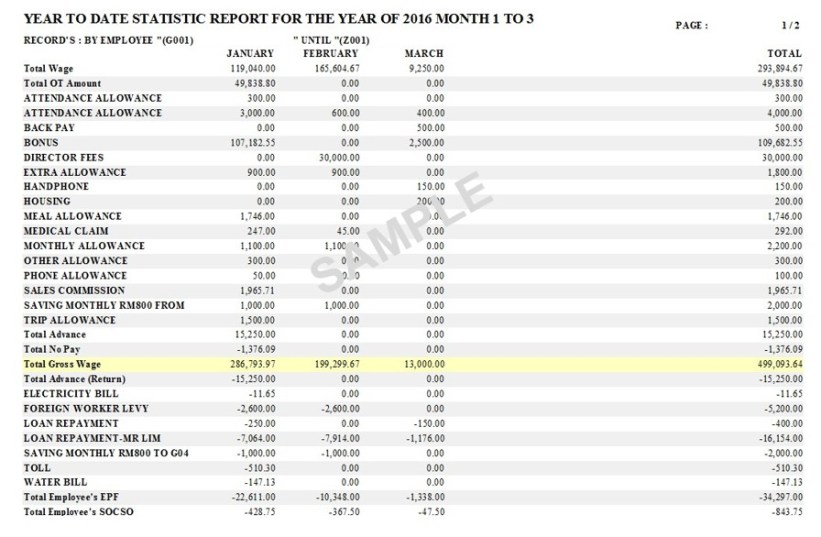

| Payroll Summary Report(U) | Statistic Report |

| Overtime Summary Report | Year To Date Payroll Summary Report |

| Overtime Summary Report in Details | Year To Date Overtime Summary Report |

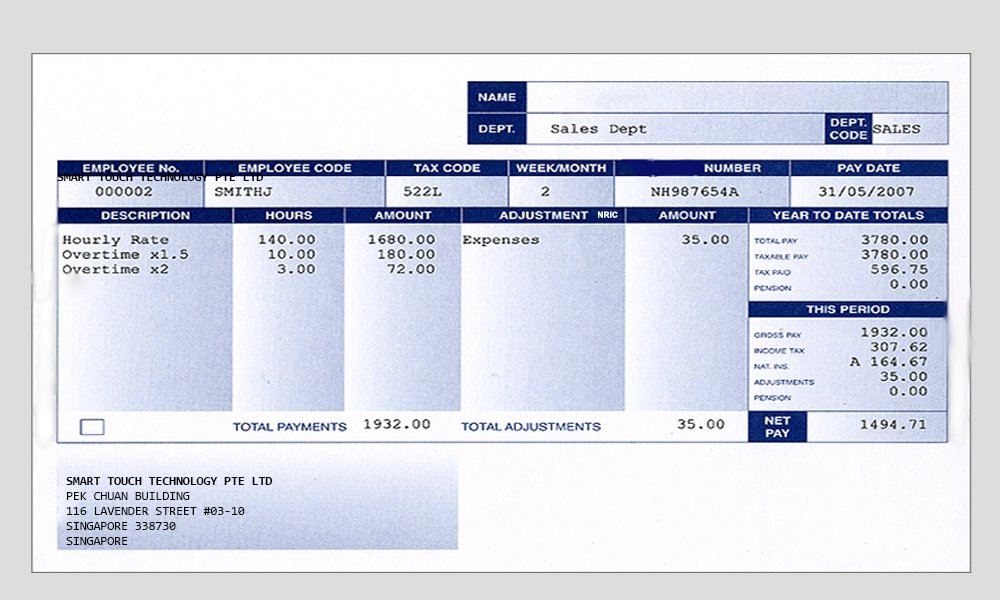

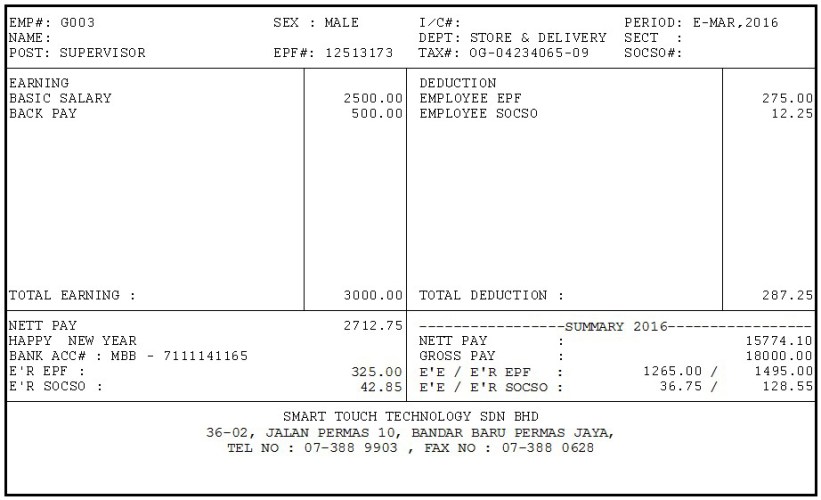

Sample of Reports

Payslip Template for Singapore HRMS and Payroll Software

Payslip is a small document generated using Singapore HRMS and Payroll Software like Smart Touch’s Singapore by a company to show the facts about the pay of employees in details. Payslip must include both description and numerical data about the salary of an employee along with other information, such as; name of employee, his or her designation, name of employer, date of pay, month of pay, name of company.

To all appearance, a format for pay slip should be drafted as a professional manner, because a pay slip is significantly beneficial for employee as it’ll helps him to keep it as proof of having pay. Apart of this, a pay slip template will makes sure that employer has granted the pay to specific employee on certain date. Thus, this slip will use to account the right tax code of employee; seemingly it’ll also assist the employee when he’s applying for an insurance policy.

Items in Payslip for Singapore HRMS and Payroll Software

| Item Description in Payslip |

| Full name of employer. |

| Full name of employee. |

| Date of payment (or dates, if the pay slips consolidates multiple payments). |

Basic salary: For hourly, daily or piece-rated workers, indicate all of the following: -Basic rate of pay, e.g. $X per hour. -Total number of hours or days worked or pieces produced. |

| Start and end date of salary period. |

Allowances paid for salary period, such as: -All fixed allowances, e.g. transport. -All ad-hoc allowances, e.g. one-off uniform allowance. |

Any other additional payment for each salary period, such as: -Bonuses -Rest day pay -Public holiday pay |

Deductions made for each salary period, such as: -All fixed deductions (e.g. employee’s CPF contribution). -All ad-hoc deductions (e.g. deductions for no-pay leave, absence from work). |

| Overtime hours worked. |

| Overtime pay. |

| Start and end date of overtime payment period (if different from item 5 start and end date of salary period). |

| Net salary paid in total. |

Sample of Payslip Template

Contact Information

Reach us at : 116, Lavender Street, Pek Chuan Building #03-10, Singapore 338730.

Send us a mail : sales@smartouch.com.sg

For Enquires please contact: